Navigating the complexities of annuities can be a daunting task, especially when annuity Market Value Adjustments come into play. These adjustments are crucial for retirees, financial planners, insurance professionals, and anyone involved in the world of financial planning. We will demystify annuity Market Value Adjustments (MVAs), explore their impact on annuities, and provide practical insights to help you make informed decisions.

Annuity Market Value Adjustments - What Are They?

What is a Market Value Adjustment (MVA)?

A Market Value Adjustment (MVA) is a feature found in some fixed annuities that adjusts the value of your contract based on current interest rates. This adjustment can either increase or decrease the amount you receive if you withdraw funds before the end of your annuity's term; in other words, if your withdrawal is subject to surrender charges, it’s likely also subject to an MVA. The MVA aims to protect insurance companies from interest rate fluctuations, though when rates decline, the MVA can provide more funds to the policyholder on withdrawals that are subject to surrender charges.

Purpose of MVAs

The purpose of an MVA is to protect insurance companies from interest rate risk and to reflect the current market environment in the event of early withdrawals, especially when surrender charges apply. The adjustment is typically calculated using a formula specified in the annuity contract.

When Interest Rates Change

When market interest rates rise, the MVA may reduce the amount you receive. Conversely, if interest rates drop, the MVA could increase your withdrawal amount. The MVA mechanism operates this way due to the widely-known financial present value concept that the market value of a bond goes down when interest rates rise while its market value goes up when rates decline. Understanding how an MVA works is essential for anyone considering an annuity, as it directly affects your investment's value.

Bigger Impact in Long-Term Annuity Contracts

MVAs are particularly relevant for long-term contracts, where interest rate changes over time can significantly impact the value of your contract and any withdrawals you make before maturity that are also subject to surrender charges. Consulting with an annuity expert and knowing the basics of MVAs can help you better plan your financial future and make more informed decisions about your annuity investments.

How Does an Annuity Market Value Adjustment Work?

An annuity Market Value Adjustment (MVA) works by comparing the interest rate environment at the time of your withdrawal to the rate environment when you purchased the annuity; the rate environment is typically measured by the yield on a specific benchmark credit index that’s used as a reference per your annuity contract. If you withdraw funds when market interest rates are higher than when you bought the annuity, the MVA will typically reduce your payout. Conversely, if rates are lower, the MVA may increase your payout.

The adjustment is calculated using a formula specified in your annuity contract. This formula considers the difference between the current market interest rate and the rate at the time of purchase. It's important to review your contract to understand how the MVA will be applied in different interest rate scenarios.

For instance, if you purchased an annuity when the interest rate was 3% and decide to withdraw funds when the rate is 4%, the MVA will likely reduce your withdrawal amount. On the other hand, if the rate drops to 2% from 3%, the MVA could increase your withdrawal amount. This mechanism helps insurance companies manage the interest rate risk in their investment portfolios while offering competitive annuity products.

How Do I Calculate An Annuity's Market Value Adjustment? A Real World Example

Calculating an annuity Market Value Adjustment involves a specific formula that varies by insurer. Generally, the formula considers the difference between the guaranteed interest rate in your contract and the current market rate, which could be approximated by looking at the change in the rate on a reference credit index. Additionally, the MVA factors in the duration left in the annuity's term.

For example, here’s a real life MVA formula that is used by annuity carrier Aspida on one of their 3-year fixed annuity products called Synergy Choice MYGA 3. (Note: Different carriers and products have their own formula variations per the annuity contract to calculate MVAs, and such formulas can change.):

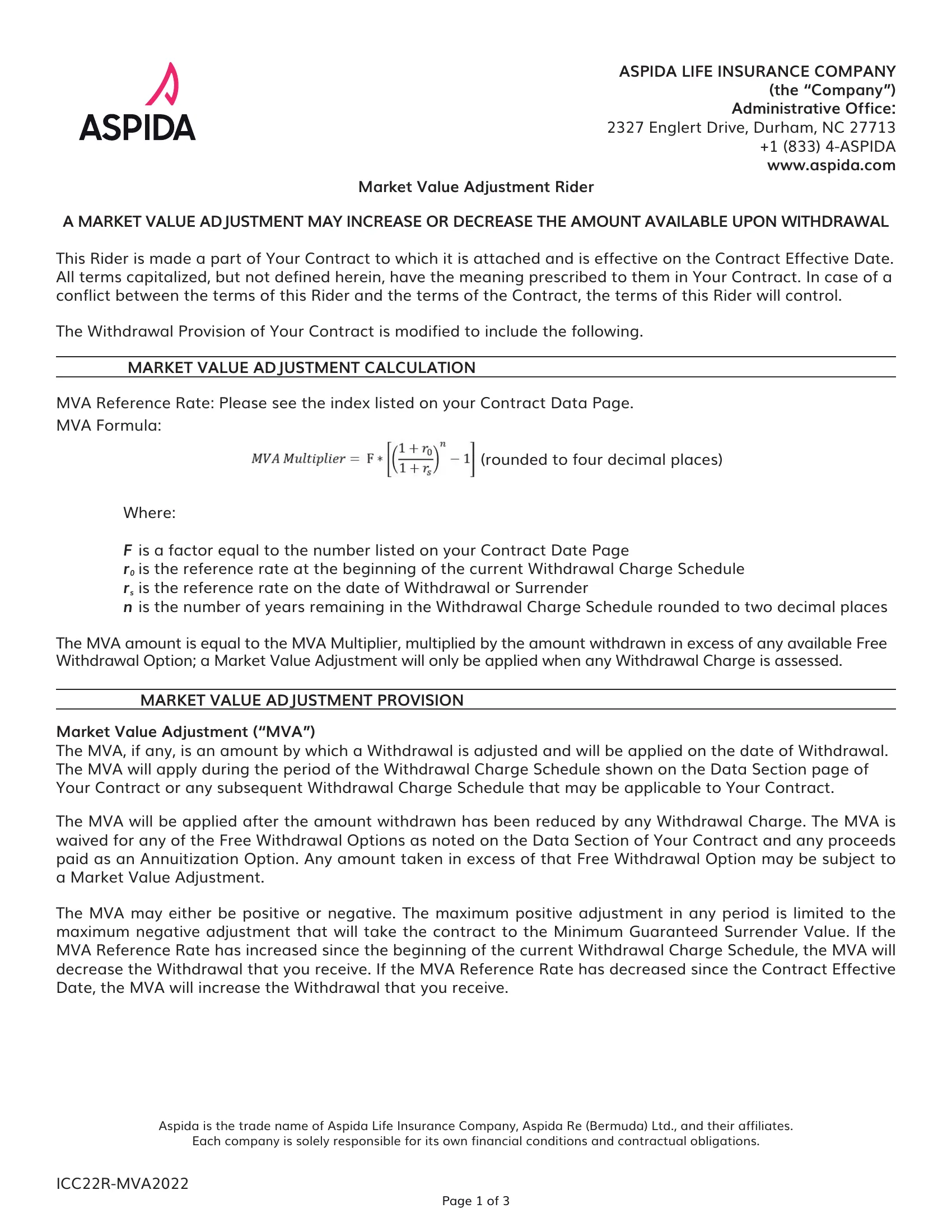

Market Value Adjustment (MVA) Calculation

Here is a real example of a relevant formula from the Aspida Synergy Choice MYGA 3 contract (Contract ID: ICC22C-MYGA1012, Section: ICC22R-MVA2022):

MVA Multiplier = F * [(1 + r0) / (1 + rS)]^n - 1 (rounded to four decimal places)

The MVA adjustment amount is equal to the MVA Multiplier multiplied by the amount withdrawn in excess of any available Free Withdrawal Option; a Market Value Adjustment will only be applied when any Withdrawal Charge is assessed.

Where:

- F is a factor equal to the number listed on your Contract Data Page

- r0 is the reference rate at the beginning of the current Withdrawal Charge Schedule

- rS is the reference rate on the date of Withdrawal or Surrender

- n is the number of years remaining in the Withdrawal Charge Schedule rounded to two decimal places

MVA Reference Rate: ICE BofA 3-5 Year US Corporate Index Effective Yield

An Example to Illustrate How This Works

- Let’s assume that you withdrew $10,000 above the Free Withdrawal Option amount

- MVA Reference Rate at issuance was 5.50%

- MVA Reference Rate at withdrawal is 4.50% (so rates are now lower)

- There are two years remaining in the Withdrawal Charge Schedule

F = 1

r0 = 5.50% = 0.055

rS = 4.50% = 0.045

n = 2

MVA Multiplier = 1 x [(1 + 0.055) / (1 + 0.045)]^2 - 1

= (1.0095)^2 - 1

= 0.0192 (rounded to four decimal places)

The MVA Multiplier would thus be equal to 0.0192.

Therefore:

MVA adjustment amount = MVA Multiplier x Amount withdrawn above Free Withdrawal Option

= 0.0192 x $10,000

= $192

In other words, the $10,000 amount that you withdrew above your Free Withdrawal Option, net of the Withdrawal Charge, has gone up by a positive $192. You are receiving more money than if there had been no MVA adjustment.

This means that when interest rates have generally gone down from the time your annuity was issued to the time of the withdrawal before maturity, the MVA or Market Value Adjustment can actually work in your favor when withdrawing funds from your account above the Free Withdrawal Option amount.

In this example, the MVA reference rate has gone down 1.00% from 5.50% at issuance to 4.50% at withdrawal, and there are two years remaining on the surrender or Withdrawal Charge Schedule. This results in an MVA Multiplier of 0.0192, which is then applied to the amount withdrawn above your Free Withdrawal Option.

In our case, this means that for every $10,000 withdrawn above the Free Withdrawal Option, you will receive an additional $192 due to the positive MVA adjustment, net of Withdrawal Charges. If interest rates have gone up, then the opposite is true; you’d be getting less money, net of surrender charges.

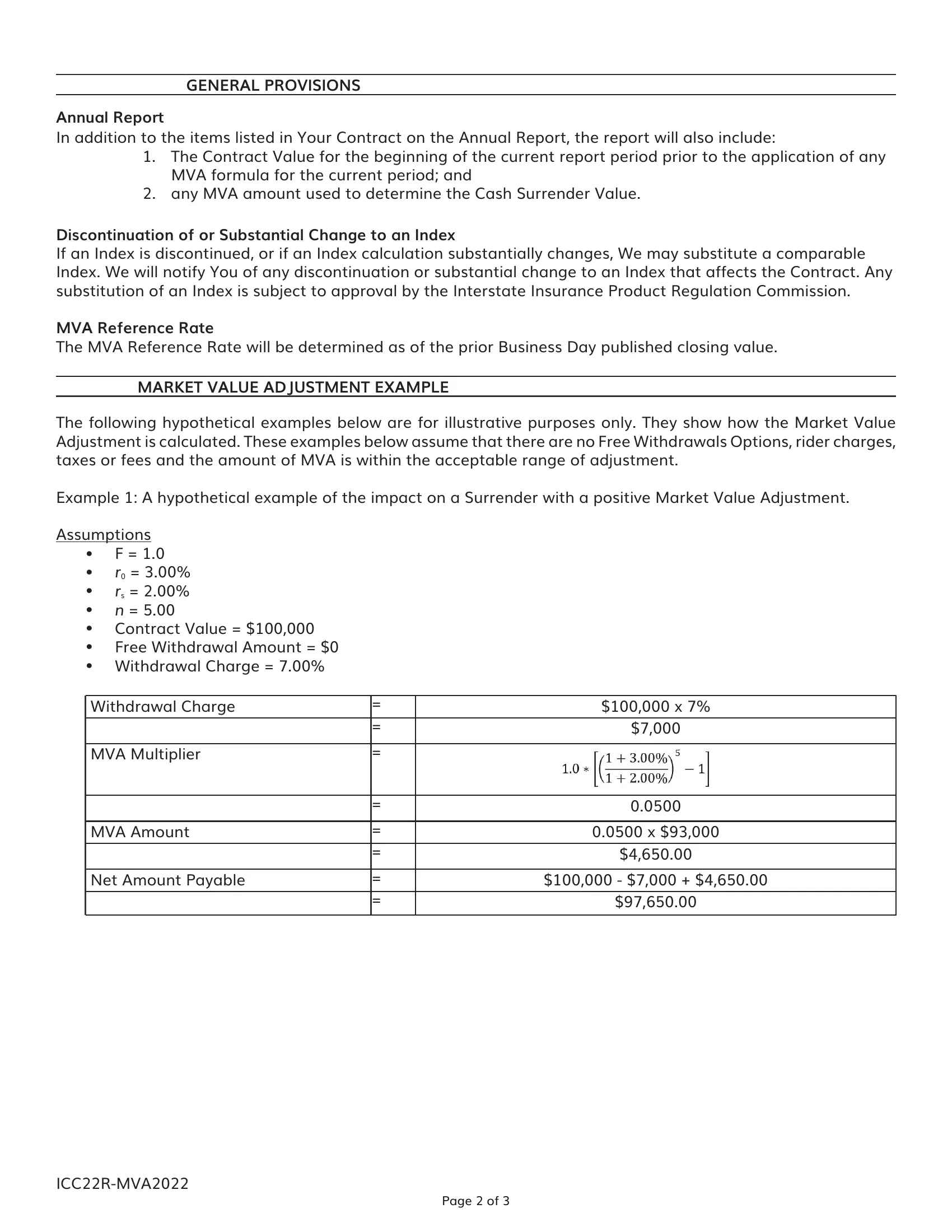

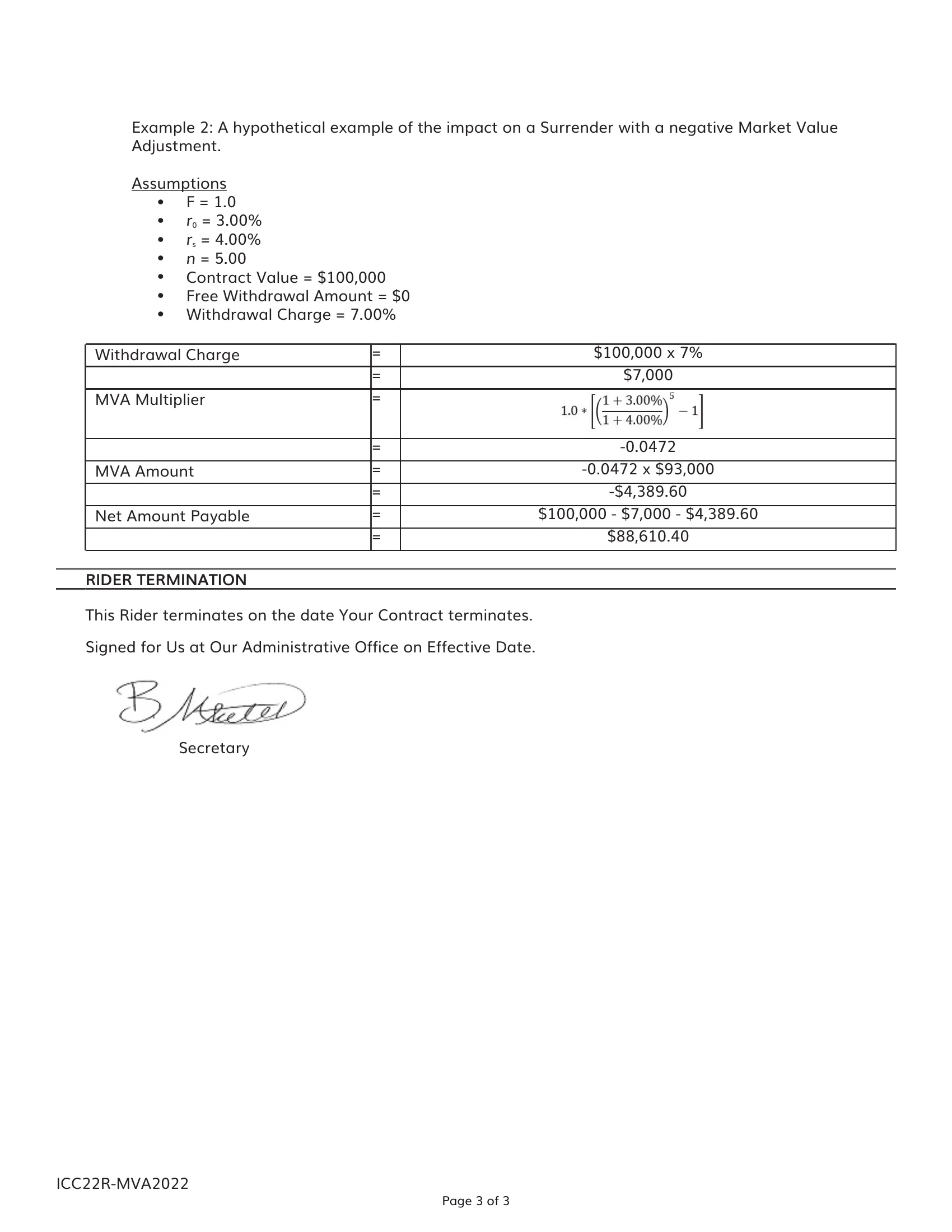

Examples from Aspida's Synergy Choice Fixed Annuity Contract

See below a few pages from the Aspida Synergy Choice 3 contract regarding the MVA formula used and several example calculations (Source: Contract ID: ICC22C-MYGA1012, Section: ICC22R-MVA2022):

Does an MVA Apply to Free Withdrawals from My Annuity?

Many annuity contracts allow for "free withdrawals," typically up to a certain percentage of the contract value each year or interest accumulated in the prior 12 months. These withdrawals are usually not subject to MVAs, providing flexibility for accessing funds without penalty.

However, it's essential to review your annuity contract to understand the specific terms and conditions. Some contracts may have restrictions or conditions that could trigger an MVA even for free withdrawals.

By understanding the terms of free withdrawals, you can strategically plan your finances and avoid unnecessary penalties. Consulting with a financial advisor can help you navigate these complexities and make the most of your annuity contract.

Are All Annuities Subject to Market Value Adjustments?

Not all annuities have MVAs. Fixed annuities and indexed annuities commonly include this feature, while variable annuities typically do not. It's essential to review your annuity contract to determine if an MVA applies.

Understanding whether your annuity is subject to an MVA can help you plan your financial strategy more effectively. If your annuity includes an MVA, knowing how it works and its potential impact on your investment is crucial.

Consulting with an annuity expert can help you make informed decisions, and their guidance can be invaluable in managing your financial planning and achieving your long-term goals.

Can I Avoid an Annuity Market Value Adjustment?

There are several strategies to avoid or minimize the impact of an MVA. One approach is to plan withdrawals around the annuity's term, avoiding early withdrawals that trigger the adjustment. Another strategy is to take advantage of free withdrawals, which are typically not subject to MVAs.

Additionally, some annuity contracts offer features that allow for penalty-free withdrawals under specific circumstances, such as medical emergencies or long-term care needs. Reviewing your contract and understanding these provisions can help you avoid unnecessary penalties.

Death Benefits Typically Do Not Have MVAs

By planning your withdrawals strategically and taking advantage of available options, you can incorporate the impact of potential MVAs, positive or negative, on your annuity investment.

Factors Influencing Annuity Market Value Adjustments

Several factors influence the magnitude of an MVA, including:

- Interest Rate Changes: The difference between the initial and current yields on the reference credit index named in your contract; it’s possible the MVA formula may look instead at the current market rate and the initial guaranteed rate on your annuity.

- Duration: The remaining term of the annuity contract.

- Amount Withdrawn: The size of the withdrawal relative to the contract value.

Understanding these factors can help you estimate the potential impact of an MVA on your annuity. By being aware of these variables, you can make more informed decisions about withdrawals and manage your investment effectively.

Why Do Interest Rates Matter?

Interest rates are a critical factor in finance, influencing everything from loans and mortgages to savings and investments. They represent the cost of borrowing money and the return on savings. In the context of MVAs, interest rates determine how much your withdrawal will be adjusted.

When Interest Rates are Lower

When interest rates are lower than when you made your investment, your MVA could result in a positive adjustment. This is because the insurer benefits from reinvesting your money at a lower rate, which is less costly for them. For example, if you locked in a 5% rate but current rates are 3%, your withdrawal amount will be increased to reflect this more favorable reinvestment landscape.

When Interest Rates are Higher

If interest rates are higher at the time of your withdrawal, your MVA will likely result in a negative adjustment. The insurer faces a disadvantage by reinvesting your money at a higher rate, costing them more. For instance, if you locked in a 4% rate but current rates are 6%, your withdrawal amount will be decreased to compensate for this discrepancy.

Is There a Limit to How Much the Market Value Can Be Adjusted?

Some annuity contracts include caps or limits on the MVA to protect investors from extreme fluctuations. For instance, most annuity contracts specify a minimum guaranteed surrender value, ensuring that the MVA cannot reduce the surrender value below a certain level, preventing big losses due to market fluctuations. These limits ensure that the adjustment remains within a specified range, providing a level of predictability and security.

Understanding the limits, if any, on your annuity's MVA can help you plan your financial strategy more effectively. By knowing the maximum potential impact, you can make more informed decisions about withdrawals and manage your investment more confidently.

Reviewing your annuity contract and consulting with an annuity agent or expert can provide clarity on the specific limits of your MVA. This guidance can be invaluable in optimizing your financial strategy and achieving your long-term goals.

How Often Are Market Value Adjustments Applied to an Annuity?

MVAs are typically applied only when you make a withdrawal or surrender the annuity before the end of the term; if there are free withdrawals available on your annuity, then the MVA and surrender charge would typically only apply to the withdrawal amounts in excess of your free withdrawal amount. The MVA reflects the interest rate environment at the time of the transaction, ensuring the contract's value aligns with current market conditions.

Understanding the frequency of MVAs can help you plan your financial strategy more effectively. By being aware of when these adjustments apply, you can make more informed decisions about withdrawals and manage your investment more confidently.

Do All Insurance Companies Use the Same Method for Calculating MVAs?

Different insurance companies may use various formulas and methods for calculating MVAs. While the general principles remain consistent, specific details can vary significantly between providers.

Can I Replace or Transfer My Annuity If It Has a Market Value Adjustment?

While replacing or transferring an annuity with an MVA is possible, the adjustment may impact the transaction's value. The MVA will be applied based on current interest rates, potentially increasing or decreasing the amount of the exchange, replacement or transfer.

Review your annuity contract and consult with a professional who can provide clarity on the specific terms and conditions of your MVA to help you optimize your financial strategy and achieve your long-term goals.

Conclusion

Annuity Market Value Adjustments (MVAs) play a significant role in the world of annuities, impacting the value of your annuity and any withdrawals from it that have surrender charges, based on current interest rates. Understanding how MVAs work, their impact on your annuity contract, and strategies to manage them effectively can help you make more informed decisions and optimize your financial planning.

By being aware of the factors influencing MVAs, you can better estimate their potential impact and plan your withdrawals strategically. In short, if you believe rates will be going down, that is in your favor as future MVAs would likely be a positive adjustment, offsetting some of the surrender charges applied to any withdrawals before the annuity matures. Talk to us at PlanEasy to learn more and be better informed.

If you're considering an annuity with an MVA, take the time to review your contract thoroughly and consult with an expert with deep domain knowledge about annuities. This proactive approach will empower you to make informed decisions and maximize the benefits of your annuity.

Learn more and take control of your annuity strategy today. If you have any questions or need further assistance, don't hesitate to reach out to PlanEasy’s team of annuity experts, who are here to help you every step of the way.

Sources:

- Aspida Synergy Choice 3 Contract ID: ICC22C-MYGA1012, Section: ICC22R-MVA2022

- Ameritas: What Is a Market Value Adjustment?

- Annuity.org: Market Value Adjustment

- Morgan Stanley: Understanding Fixed Annuities

- Alabama Department of Insurance: Annuity Disclosure

- Wisconsin Office of the Commissioner of Insurance: Annuity Buyers Guide

- NAFA: Annuity Features Article